Insights

25min reading time

Disclaimer: This insight article is written in cooperation with the IMPACT FESTIVAL .

The economic potential of circular economy

While this model of value chain has been the keystone of the economic growth for decades, the prodigal nature of such expenditures is causing a serious global concern. Only 8.6% of global resources get recycled and reused, with the global circularity gap widening year by year. According to the Global Resources Outlook report, our use of resources has tripled since 1970 and is expected to double in the next three decades. Given the volatile and rapidly growing prices of the resources, continuously increasing consumer demand, all while the excessive carbon emissions accentuate the climate change and fossil fuel depletion, the need for a more sustainable economic model is pressing.

Sustainability & financial impact of circular economy

Based on the principle of value preservation, reduction of the material input and extended service-life of goods, Circular Economy offers substantial advantages to the traditional value chain. The driving force behind it is that circular economy benefits the environment while generating positive financial results, boosting competitiveness and building resilience. Since the premise of a circular economy is to loosen the ties between the economic growth from resource use, the model is essentially underpinned by a transition to renewable energy and materials.

The heavy reliance of manufacturing firms on materials and components not only creates a competitive disadvantage, but causes a drastic environmental impact. McKinsey Center for Business and Environment suggests that the circular model has the potential to alleviate the consumption of primary materials to drop by 32% by 2030 and by over 50% in 2050.

At the same time, in a circular scenario, similarly positive effects can be observed across multiple sectors. By 2030, the carbon-dioxide emissions could drop as much as 48% and 83% by 2050. These emissions cuts would be primarily sourced by electric, shared, and autonomous vehicles, reduced food wastage, regenerative food chains, passive housing, urban planning, and renewable energy.

Apart from reducing the use of resources and cutting global greenhouse gas emissions, circular economy strategies also open up substantial financial benefits. Research shows that there is a USD 4.5 trillion economic opportunity created by circular economy. By focusing on reuse, repair, remanufacturing and sharing, new business models present significant innovation opportunities.

For instance, when it comes to the plastic economy, which almost entirely relies on feedstocks and nonrenewable resources, the circular system offers an essential solution. The current volume of plastic pollution leads to USD 13 billion in annual costs and economic losses. Using the resource benefits of circular economy to transform the future of plastic could result in a significant economic-multiplier effect. By reducing the pollution and toxic emissions that come from plastic waste, the healthcare costs would decrease. At the same time, reducing fossil fuel use for plastic production would help mitigate climate change and its associated costs.

Growing interest in circular economy investments

Although, circular economy entails major economic and environmental benefits, its investment potential has remained relatively untapped. Recently, however, the economic opportunity of the circular model is becoming more widely recognized among the stakeholders of the financial services industry. Examples of the US-based BlackRock and Swiss peer, RobecoSAM, show that world’s largest investors started to launch specialized circular equity funds. Overall, the global trend reflects that the managed assets in public equity funds with a focus on the circular economy have grown from USD 0.3 billion to USD 8 billion in 2021, demonstrating a 26-fold in less than 2 years.

Index providers are now also expanding within the circular landscape by launching more CE-specialized products. The index provider, Solactive, established a sharing economy focused index, while Morgan Stanley Capital International (MSCI) introduced a CE and renewable energy index. Most recognized among others, the ECPI group, launched a Circular Economy Equity Leader Index. This specialized index compromises categories that include circular supplies, resource recovery, product life extension, sharing platforms, and product as a service.

Barriers to invest in a circular economy

We can already observe a growing interest in the As we have discussed in the first article of this series, there are many barriers that companies need to overcome to create a circular ecosystem. A main barrier is the lack of funding, even if there is currently a growing financial interest to invest in circular economy business opportunities. However, only leaving it at the financial barriers would not be neosfer-like! We will go to the bottom of what reduces the amount of money invested into circular solutions. First, some of the biggest market imperfections are highlighted before barriers that trigger these imperfections are analyzed.

Market imperfections

When talking about problems with money flow into a circular economy, one must start by analyzing what is missing from product prices in a linear economy: unpriced positive and negative externalities. Greenhouse gas (GHG) emissions, related health hazards and subsequent environmental pollution are often not priced into regular linear product prices. This puts CE in a disadvantaged position. A circular investment, taking into consideration all social costs of production and consumption is doomed to a lower return compared to linear business models reflecting mere production costs.

Moreover, financial markets are far from picture-perfect. Generally speaking, there can be a short-termism observed when investment decisions are made additionally to market frictions through subsidies which leads to a lack of liquid, long-term capital for circular investments. Furthermore, psychological biases like the home-bias, incentive-caused biases, an oversimplification tendency, hindsight bias and the bandwagon effect can lead to harmful behavior when it comes to financing circular economy.

As the concept of circular economy and the reporting standards for showing how successful circular solutions can be, are still in its starting point, the lack of objective information or asymmetric information is another issue. As financial institutions require a large amount of information to take investment decisions, the lack of it might also lead to resistance to finance CE.

These existing market imperfections reduce the potential measured profitability of investing into circular businesses via a reduced return of investments or via increased risks associated with the investment for investors. To better understand new ways of financing circular economy, we quickly want to describe the barriers that in return create these market imperfections.

Barriers that trigger market imperfections

Circular investments require large upfront costs of first creating an infrastructure for these solutions to work. This is especially challenging for micro, small and medium enterprises (MSMEs), which are more sensitive than large enterprises to these costs. On paper, these infrastructure investments reduce the attractiveness of investments for investors.

As the market for circular economy investments is still quite new, and return-based finance requires a degree of certainty that the project / promoter can generate cash flows in the future, these uncertainties can create the biases we highlighted above.

Missing credible commitments by public authorities (governments) are posing additional risk on (long-term) investment decisions for private sector actors. As we showed in our first article, there are already some governmental efforts regarding financing and creating circular ecosystems. However, there are still not enough credible commitments. Besides this issue, the political landscape with trade wars, geographical clashes and wars leads to harmful environments for investors that can lead to under-financing of circular economies.

Financial instruments to promote circular economy

When observing the Sustainable Development Goal (SDG) targets, Nationally Determined Contributions (NDCs) set in the Paris Agreement and the new circular economy action plan (CEAP) of the European Commission (EC) different circular investment priorities can be identified. They all require a mix of instruments and measures across all sectors and material flows to increase investments in circular economies and to avoid and reduce the market imperfections that are in place at the moment.

Investments in a circular enabling framework

Investment in sector relevant regulation, assistance in formulating policies of regulators and institutions in the financial sector, development of skills, demand analysis. Those framework conditions determine the time frame and the amount of financial and technical resources required. A systematic pricing-in of various environmental damages related to linear activities would presumably boost circular businesses through appropriate price signals. Additionally, to reducing externalities reflected in prices, creating reporting standards for circular businesses and picking up some standardized reporting measures would reduce asymmetric information and biases that hinder the increase in circular investments. In the later stages of the article, we precisely analyze potential measurements of the impact that circular businesses can generate and that could be picked by regulators as standardized impact measurements.

Investments in circular economy related assets

Investment in productive assets is a prior obligation for supporting the circular economy. Access to adapted finance for those assets, through CE-aligned loan finance, equity injections, leasing agreements as well as risk mitigation instruments, is essential. With the next section, we want to focus on these financial instruments and especially highlight equity, debt and mixed instruments to increase the investments in circular businesses.

To better understand and categorize the selection of financial instruments, we first must look at the stage of development or bankability a circular solution is located in. The degree of concessionality – the level of benefit provided to a borrower when compared with financing available at full market rates – should increase proportionally to the magnitude of the barriers to implementation. Equity financing, debt financing and mixed instruments are typically related to the three common stages of corporate development:

- Proof of Concept (PoC) for innovative projects, R&D, new technologies, products, or services: equity and grants,

- Commercialization: a combination of grants, equity financing and subordinated loans,

- Scale-up: equity and debt financing

Equity

For small projects, own funds might be enough to invest in project assets such as efficiency equipment. In case of large projects, developers need to mobilize sufficient equity, most often through interested investors (private equity) or through the listing of the company on the public markets (public equity). Equity investments have the potential for high returns but are associated with higher risks. These investors typically invest in the two later stages of corporate development.

There are already multiple private equity investors active in the circular ecosystem:

BlackRock, Candriam, Crédit Suisse and ROBECO, among others, offer private equity targeting CE projects, particularly in Europe through equity funds. Furthermore, BNP Paribas provides a CE-based exchange-traded fund (reflecting the CE Leaders Equity Index).

The private equity Leadership Fund by Closed Loop Partners targets USD 300 million and focuses on acquiring CE-relevant companies.

Next to private equity investors, venture capital firms additionally target investments in the PoC stage and focus on circular companies in early stages of their development. This involves a high risk of failure, which consequently leads to the highest return expectations. The typical investment horizon is less than 10 years which are not in favor of circular activities, given their naturally long-term materialization of revenues.

However, there are more and more venture capital firms willing to invest and take that risk:

Empower all consumers in the fight to reclaim our planet. This is the motto on the homepage of Regeneration.VC, a new venture capital company that has recently closed a first round of 45 million dollars for the cause. Backed by Leonardo DiCaprio, the VC focuses on circular and regenerative economy.

Even bigger investments have already been made by the VC private equity Plastics Fund 1 by Archipelago Eco Investors. The fund targets EUR 100 million for impact investments in SMEs that are developing alternatives to single use plastic packaging or recovering value by recycling in a circular model.

Additionally, the Closed Loop Partners’ Closed Loop Venture Fund provides early-stage capital for companies that work among the Value Hill Approach for increased productivity and recycling.

Debt - Loans

Debt finance instruments (e.g. lending) typically consist of loans provided by banks or financial institutions. Institutional investors and bonds issued by corporates or public authorities and sold to investors to raise fixed-income capital.

In general, lenders are more risk-averse than equity investors and require more securities or target the later development stages of circular businesses. While commercial loans tend to focus on more conservative risk-return calculations, concessional loans with more favorable terms (longer-term maturity, and longer grace period) offer opportunities for circular business models.

We want to give you examples of public and private financial organizations that work with concessional loans to finance the circular economy. As you will shortly see, this debt financing instrument is moving way more money to the circular ecosystem compared to equity financing.

One public institution investing in circular models is the European Bank for Reconstruction and Development. Their Circular Economy Regional Initiative includes concessional co-financing in Turkey, Albania, Bosnia-Herzegovina, and other countries and focuses on the management of raw materials during the lifecycle of different products.

The second public institutions we need to highlight is the European Investment Bank (EIB). The EIB reports about EUR 2.5 billion in lending for circular projects over the last five years, such as collection and recycling infrastructure for Waste Electrical and Electronic Equipment.

One private banking group in Italy, Intesa Sanpaolo, takes an innovative approach to the lending business for circular economy. The bank manages Plafond, a dedicated credit facility (EUR 6 billion) with a focus on innovative CE projects that create solutions for lifetime extensions, regeneration of natural capital, and circular design.

One of the private companies using loans for circular economy is the chemicals’ company Indorama Ventures. They will use loans among other financial instruments to finance their commitments of USD 1.5 billion for investments in plastics recycling infrastructure.

Debt - Bonds

When a bank loan is insufficient to finance corporates or national governments, bonds can provide an alternative to attract capital. Bonds are debt securities sold to investors.

While still in their infancy, new types of thematic bonds have emerged and include sustainability-linked, climate-aligned, or transition bonds. Internationally acknowledged are green, social and sustainability-linked bonds, defined by the International Capital Market Association (ICMA). For each type of bond, the ICMA has developed principles which serve as voluntary best practice guidelines, and which are updated regularly.

European approaches to bonds are clearly stated in the new Green Bonds Standards, while more general green guidelines are stated in the EU Taxonomy. Additionally, to governments and regulators, corporations can also issue green bonds to boost their transition towards a greener and more circular future:

BASF’s green bond (EUR 1 billion) enables CE-adapted products and processes.

PepsiCo’s green bond (USD 1 billion) funds activities that lead e.g. to reduction of virgin plastic.

The World Bank’s Sustainable Development Bond (USD 10 million), also referred to as blue bonds, targets plastic waste pollution in oceans.

Mixed instruments

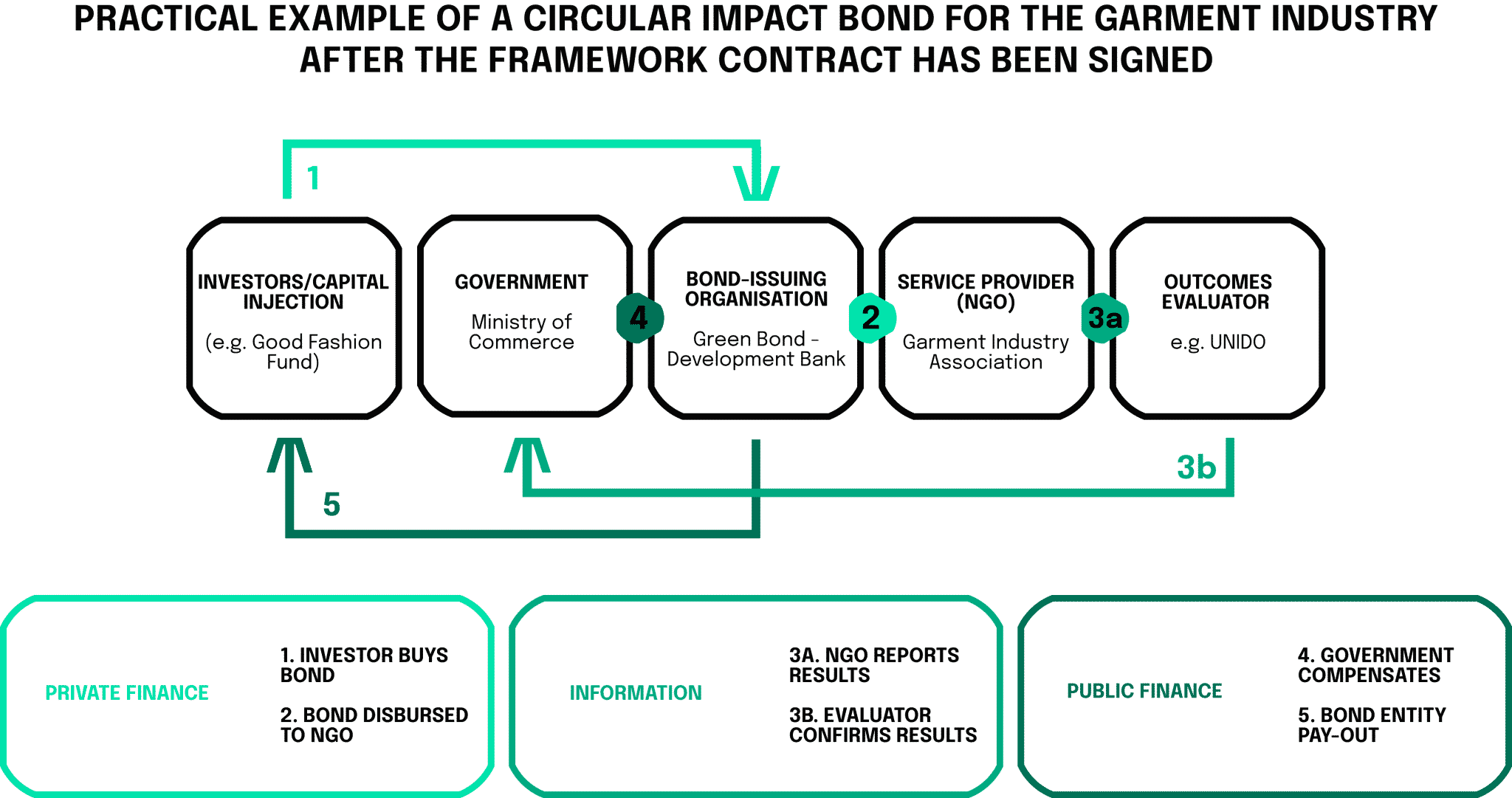

Of special importance when talking about circular bonds are social impact bonds for circular city development. In summary, provide opportunities for e.g., city governments to raise funds to invest in innovative circular city initiatives without financial risk. SIBs are issued by (sub-) national authorities, however as a small downside, there is no established financial standard yet. As these social impact bonds are a rather complex tool, and are more extensive compared to “normal” bonds, they can be seen as mixed instruments between equity and debt financing.

More generally, social impact bonds are agreements between a public authority, a service-provider, and a bond-issuing organization. It is essential that the outputs of this agreement are clearly defined. First, a social impact entity provides services against payments. Second, private investors come into play with respective capital for circular impact. Third, we need a governmental entity who can sign effective performance-based contracts. Forth, a bond-issuing organization that represents the intermediary between investors, service providers, and public authorities must be there to issue the bond. Finally, an independent evaluation actor might be used to confirm results. Thus, an investor funds a non-profit organization to produce a social outcome via the bond-issuing organization, which disburses the invested funds to the service providers for financing operating costs. In return, the public authority pays the bond issuer if circular outcomes are met. The organization in return uses the payments to reimburse the private investor and provide a positive ROI to these investors willing to take this circular risk.

Besides the rather classical approach of financing businesses, the circular economy ecosystem can also enable financing instruments that are more of a mix between equity and debt financing.

The sharing economy creates new forms of market transactions and segments. Sharing becomes increasingly popular among consumers themselves which creates Consumer to Consumer (C2C) markets. This trend is accelerated by internet technology which enables the emergence of Peer to Peer (P2P) platforms through which consumers find the products and services in the local community that are available for sharing. However, the trend towards P2P transaction can also be used to provide finance to circular businesses. P2P lending enables individuals to obtain loans directly from other individuals, cutting out the financial institution as the middleman. These agreements are conducted fully online and are largely operating in unregulated fields of the financial industry. Each website sets the rates and the terms and enables the transaction. Most sites have a wide range of interest rates based on the creditworthiness of the applicant.

For circular businesses these opportunities provide easier access to capital, but also the investment amount generally is smaller compared to more equity-focused ways of financing. For the investors, they get access to more investments projects with potential high returns. However, the risk of failure is also way larger, while the market is defined by asymmetric information and non-transparent regulations.

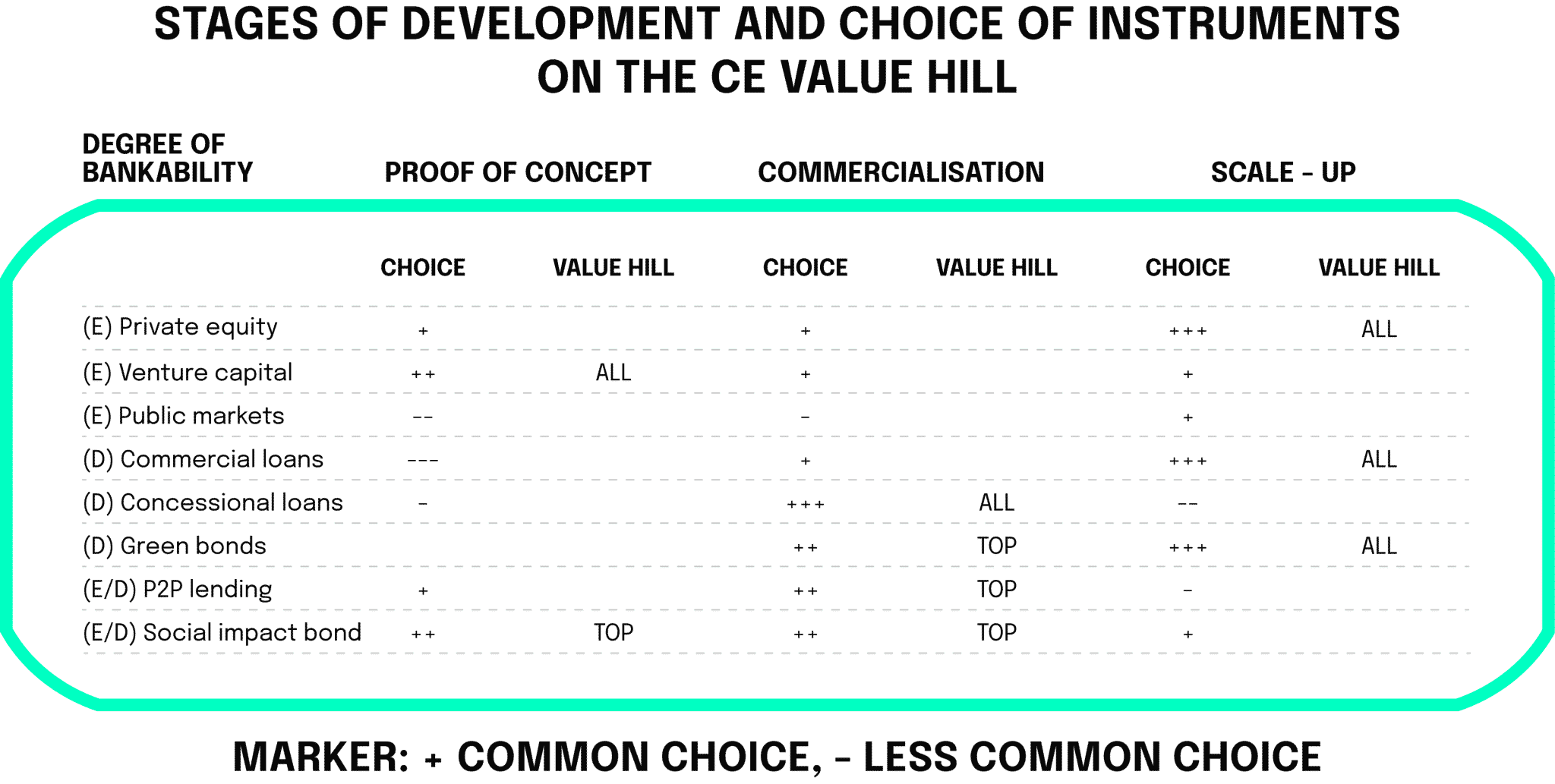

To combine the Value Hill Approach presented in the first article, the three stages of corporate development and the different financial instruments presented above, we have created the infographic below. It shows all the financial instruments and when they are best used dependent on the development stage of the circular business.

Measuring the impact of circular business activities

As we have already highlighted in the section about market imperfections, measuring circular economy activities or better, the lack of measurement, provides a large challenge. Whilst this already creates some market barriers for circular investments, if social impact bonds should play a larger role in the future, we definitely must work towards establishing KPIs to measure the effectiveness of corporate circular economy activities.

As you will shortly see, there are many frameworks of assessing circular economy impact. We will split the overview between the European Union, the national level, and the private level.

Even if the frameworks are defined and applied on the macroeconomic level, there are still implications for the individual corporation. The frameworks overall will give you indicators to take as a first step to defining your impact assessment of your circular actions.

European union

In 2018, the EU defined a Monitoring Framework for the Circular Economy. On 11 pages, the report defines 10 indicators for the development of the circular economy in the EU. The 10 indicators grouped according to the four stages of circular economy: production and consumption, waste management, secondary raw materials and competitiveness and innovation. Even if the indicators should display the progress on the macroeconomic level, they still add value for the assessment of your progress towards establishing a circular business model.

Five years earlier, the EU already started to implement the first circular measurements, namely the EU Resource Efficiency Scoreboard. The scorecard is mainly a set of resource efficiency indicators including a lead indicator on resources, dashboard indicators on materials, land, water and carbon, and theme-specific indicators. Basically, the indicators show the progress the EU is making in respect to resource efficiency. These indicators are especially important to observe, as the efficient use of resources is one of the key aspects of the Value Hill Approach and the ten aspirations of the circular economy.

National level

Besides the EU, some member states already started to analyze and implement some measure to objective the impact of their national circular activities. These indicators are different from the EU-wide ones, and have the potential to give you a different perspective on some key things to measure.

France defined 10 key indicators for monitoring their circular economy in 2017. Within their 36-page-long report, they cover the seven pillars with their indicators, ranging from domestic material consumption per person to the number of circular projects per year. The interesting thing here is that France is using a benchmarking approach and always compare their number relative to the EU numbers. This approach is especially interesting for corporations trying to show their effectiveness, comparing to their overall market is a great start.

Even earlier, in 2012 to be exact, Germany started its initiative on resource efficiency. The program is aimed to support the sustainable use and conservation of natural resources. Since 2016 uses total raw material productivity as a headline indicator.

Private level

On the private level, we see various organizations trying to establish frameworks of measuring the impact of circular activities. The indicators can be used to access the macroeconomic performance of a country overall, but also separately apply for single organizations and their setup of impact KPIs.

The company Cotec evaluated the current state of the circular economy in Spain in 2017. To accomplish this, they defined 20 indicators overall, whilst benchmarking against the EU averages as well. The most recent version got published in 2019 and is still available online.

In January 2018, the first Circularity Gap Report was published during the World Annual Forum in Davos. This first report established that our world is only 9.1% circular, leaving a massive circularity gap. It also provided a framework and fact-base to measure and monitor progress in bridging the global circularity gap. The latest report got published last year and gives plenty of insights into the different KPIs one could use to establish the current state of circular business activities.

Besides the more theoretical frameworks presented above, we quickly want to mention two really operational tools you could use to assess and create more circular solutions. The University of Cambridge provides a product-focused online self-assessment tool for businesses provides guidance based on qualitative surveys. Furthermore, the Circle Economy Circle Assessment created an online tool for businesses, focused on seven elements to improve organizational activities, and support the implementation of circular economy strategies at the company level.

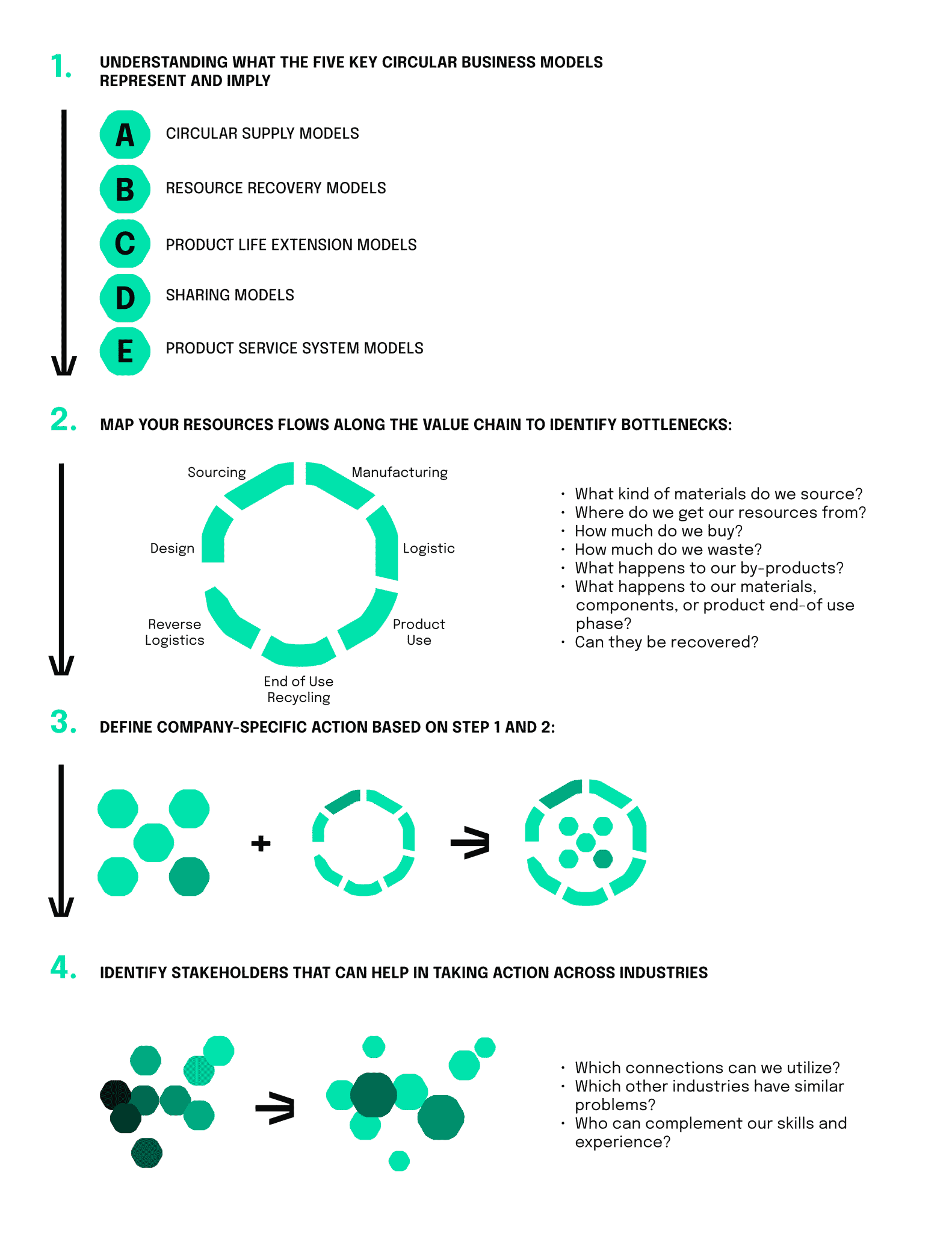

How to take circular actions?

As you now know everything about the circular economy when you combine the knowledge and frameworks from the first article and the financial instruments and potential KPIs from this article, there is one last question: How do you take circular action already today?

Aboulamer, A., Soufani, K., & Esposito, M. (2020). Financing the circular economic model. Thunderbird International Business Review, 62(6), 641–646. https://doi.org/10.1002/tie.22123

Austin, A., & Rahman, I. U. (2022). A triple helix of market failures: Financing the 3Rs of the circular economy in European SMEs. Journal of Cleaner Production, 361, 132284. https://doi.org/10.1016/j.jclepro.2022.132284

Choi, T. M., Taleizadeh, A. A., & Yue, X. (2019). Game theory applications in production research in the sharing and circular economy era. International Journal of Production Research, 58(21), 6660–6669. https://doi.org/10.1080/00207543.2019.1684593

Dewick, P., Bengtsson, M., Cohen, M. J., Sarkis, J., & Schröder, P. (2020). Circular economy finance: Clear winner or risky proposition? Journal of Industrial Ecology, 24(6), 1192–1200. https://doi.org/10.1111/jiec.13025

Dong, L., Liu, Z., & Bian, Y. (2021). Match Circular Economy and Urban Sustainability: Re-investigating Circular Economy Under Sustainable Development Goals (SDGs). Circular Economy and Sustainability. https://doi.org/10.1007/s43615-021-00032-1

The EIB Circular Economy Guide. (2020, May 1). Retrieved September 29, 2022, from https://directory.doabooks.org/handle/20.500.12854/64173

Fair, R. C. (2007). Principles of Economics. Upper Saddle River, NJ, Vereinigte Staaten: Prentice Hall.

Ghisetti, C., & Montresor, S. (2019). On the adoption of circular economy practices by small and medium-size enterprises (SMEs): does “financing-as-usual” still matter? Journal of Evolutionary Economics, 30(2), 559–586. https://doi.org/10.1007/s00191-019-00651-w

Jhomayra – Thamara, M. O., Jenny, O. O., Leonardo, I. M., & Wilman-Santiago, O. M. (2022). Circular Economy and New Technologies in Latin America as a Contribution to Sustainable Development. 2022 17th Iberian Conference on Information Systems and Technologies (CISTI). https://doi.org/10.23919/cisti54924.2022.9820303

Jinru, L., Changbiao, Z., Ahmad, B., Irfan, M., & Nazir, R. (2021). How do green financing and green logistics affect the circular economy in the pandemic situation: key mediating role of sustainable production. Economic Research-Ekonomska Istraživanja, 35(1), 3836–3856. https://doi.org/10.1080/1331677x.2021.2004437

Mähönen, J. T. (2018). Financing Sustainable Market Actors in Circular Economy. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3273263

Millette, S., Eiríkur Hull, C., & Williams, E. (2020). Business incubators as effective tools for driving circular economy. Journal of Cleaner Production, 266, 121999. https://doi.org/10.1016/j.jclepro.2020.121999

OECD. (2022). Framework for industry’s net-zero transition. OECD Environment Policy Papers. https://doi.org/10.1787/0c5e2bac-en

Zioło, M., Bąk, I., Filipiak, B. Z., & Spoz, A. (2022). IN SEARCH OF A FINANCIAL MODEL FOR A SUSTAINABLE ECONOMY. Technological and Economic Development of Economy, 28(4), 920–947. https://doi.org/10.3846/tede.2022.16632

neosfer GmbH

Eschersheimer Landstr 6

60322 Frankfurt am Main

Teil der Commerzbank Gruppe

+49 69 71 91 38 7 – 0 info@neosfer.de presse@neosfer.de bewerbung@neosfer.de