In an era where sustainability is no longer a choice but a necessity, the Corporate Sustainability Reporting Directive (CSRD) stands as a beacon guiding industries towards responsible growth. For founders and professionals, understanding the evolving landscape of sustainability reporting is crucial. The year 2023 has ushered in significant changes, particularly with the introduction of the European Sustainability Reporting Standards (ESRS), a set of guidelines that promises to reshape how businesses approach sustainability.

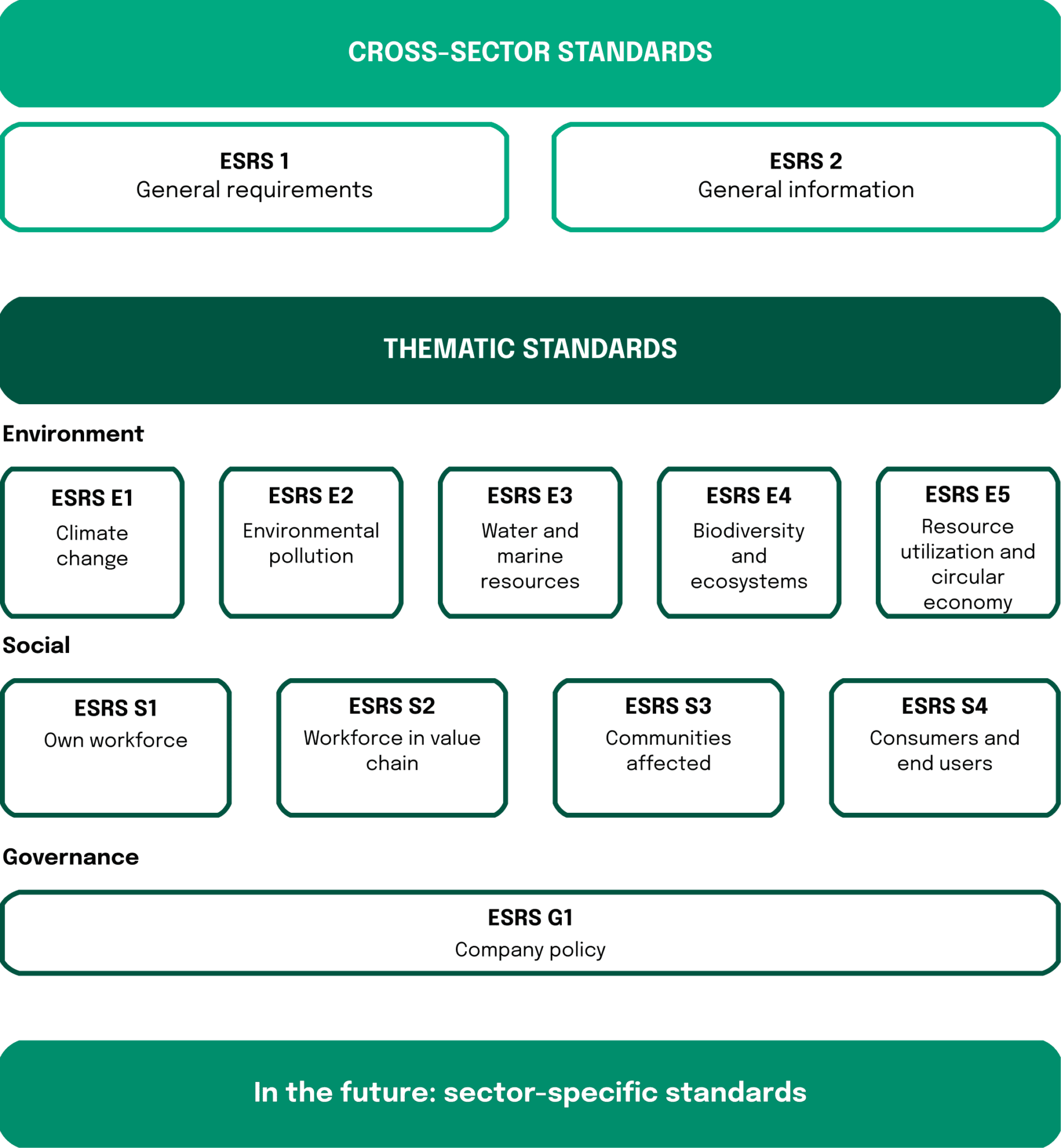

Within the European Union, the ESRS and CSRD have come together to create a comprehensive framework for sustainability reporting. The CSRD sets out the general legal requirements, while the ESRS defines the specific standards and guidelines that companies must follow to comply with CSRD. This partnership is more than a set of rules; it’s a roadmap that guides companies in disclosing sustainability information in a consistent and comparable way. For businesses, grasping the nuances of the ESRS is not just a legal necessity; it’s a strategic imperative. It’s about embracing transparency, being accountable, and aligning with a broader movement towards responsible business conduct.

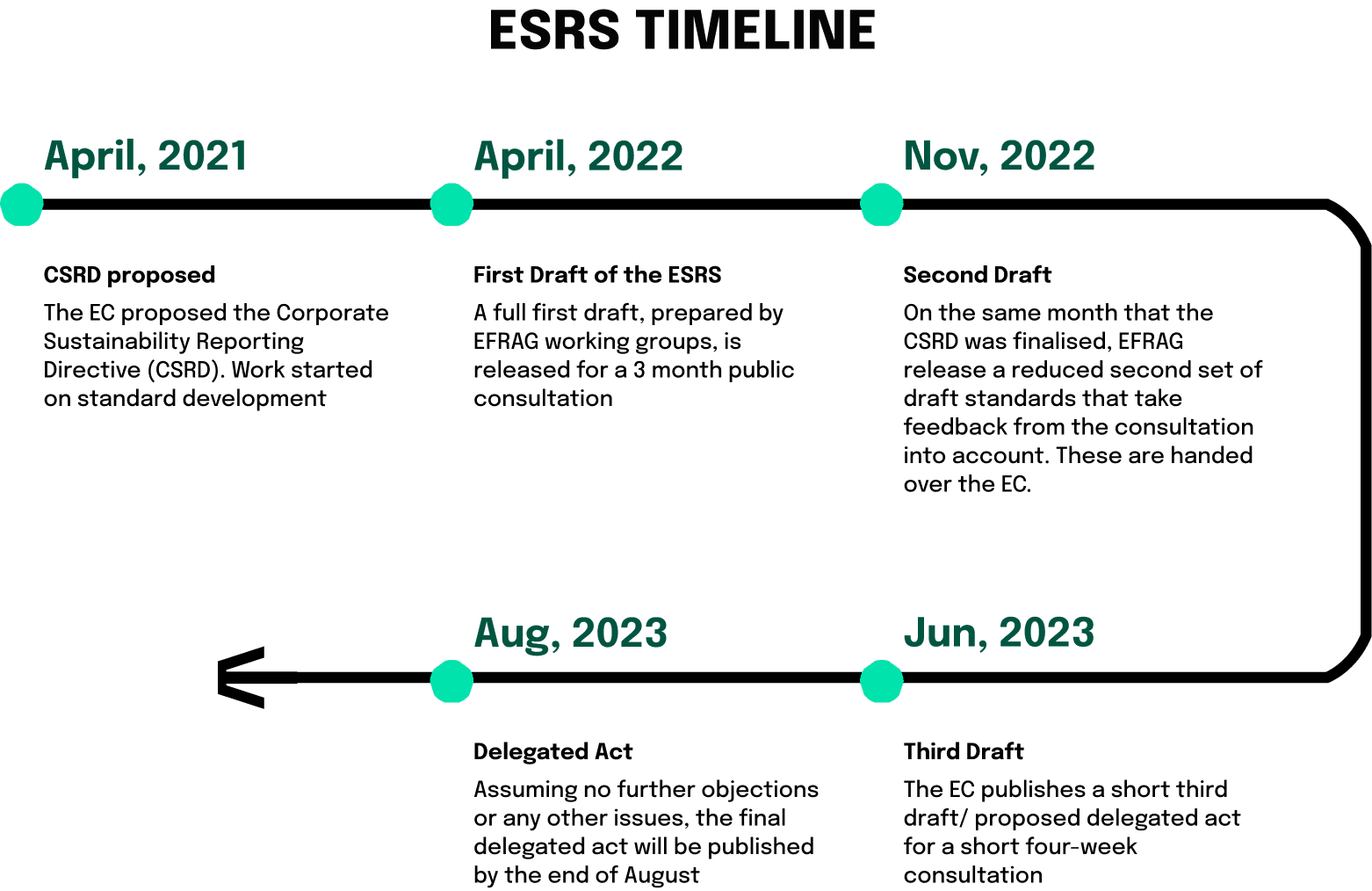

The newly proposed standards by the EU have been open for discussion and comment over the last one and a half years. In the months leading up to the publishing of the ESRS, there have been some significant changes made to the regulatory requirements.

- Material and mandatory disclosures: Under the first set of ESRS, only ESRS 2 General Disclosures includes mandatory disclosure requirements. A list of mandatory disclosure requirements (i.e. disclosures not subject to materiality assessment) has been removed, in particular related to ESRS E1 Climate Change and ESRS S1 Own Workforce. Companies must have data points to report on all topics of materiality. Within the framework of the ESRS, E1 stands out with a specific requirement: if a topic within this category is assessed as not material, a detailed justification must be meticulously provided. Conversely, for all other topic standards, the guidelines offer more flexibility, allowing entities to briefly explain the conclusions of their assessment of materiality for the given topic. Of course, we will circle back to this change when we are talking about the critique of the current ESRS guidelines.

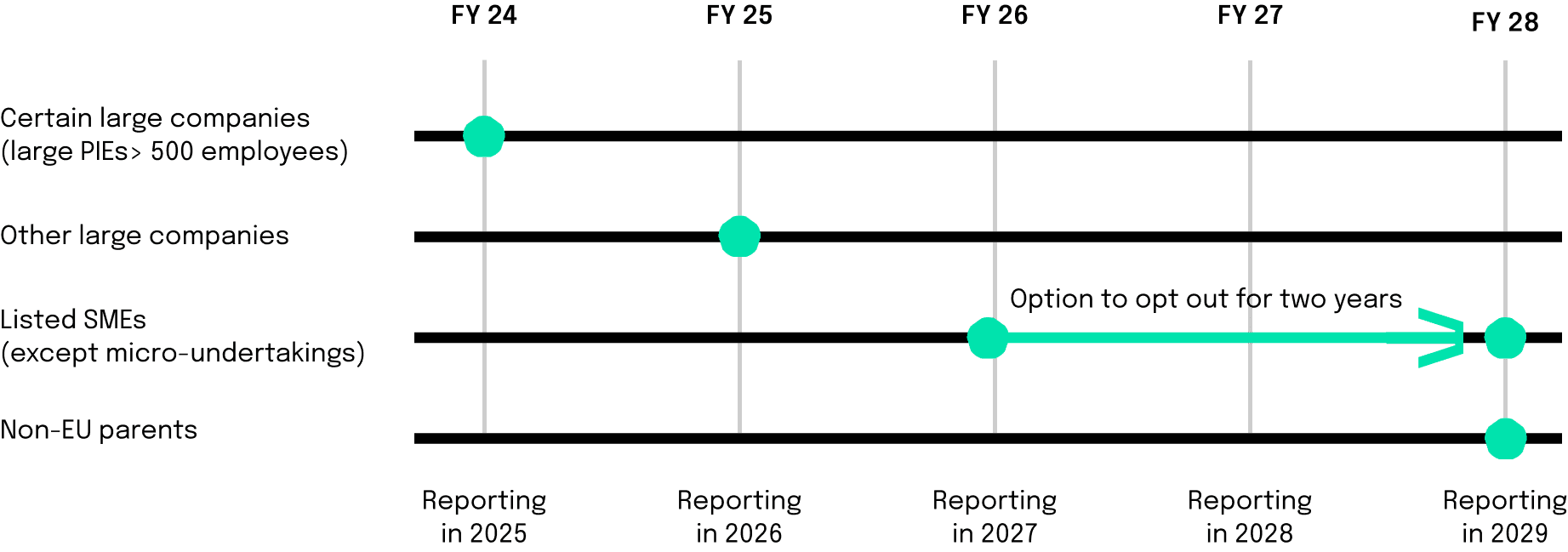

- Phase-in reliefs: as the ESRS will require significantly more areas that will be reported on, there are multiple phases in which the reporting will be implemented which can quickly be assessed in the following graphics. Additional to the implementation of the reporting requirements in steps, all companies may opt out of disclosing the expected financial impacts related to risks from environmental issues for the first year of reporting. Companies can provide qualitative disclosure only on these financial impacts for a further two years. For smaller companies (>750 employees) there are a few more facilitation in the first two years.